The Most Common Financial Mistakes Creative Businesses Make: No Tax Planning

By Paco De Leon

Welcome back to the series where we’re uncovering the most common financial mistakes that creative businesses make.

In our previous post, I debunked the expensive myth of the Delaware C Corp and how it has cost clients multiple tens of thousands of dollars.

Now, we’re exploring the same theme, taxes, but in the broader context of tax planning and how a lack of it can cost business owners in time, stress, tax overpayments, penalties for underpaying taxes, and late fees for paying them after their due date.Tax planning sounds complicated if you’ve never done it before. But the more you do it, the less daunting it gets.

Prescript: I’m not an accountant, and this isn’t tax advice. Always consult with a professional.

Taxes Are One of Your Biggest Expenses

Tax planning is essential because, as a business owner, taxes are one of your most significant expenses. Having a strategy is your best bet to making sure you’re optimizing in ways that align with you and your organization, not overpaying in taxes, incurring late fees for not paying on time, or penalties for underpaying.

And as you grow from scrappy freelancer to full-blown agency or production company, your taxes tend to move in tandem with your revenue. Establishing a tax planning habit now will only benefit you as you progress.

Some Quick Context: Accounting is ruled by the calendar

I know your excitement to dive into tax planning is bringing you to your breaking point, but before we go there, I want to lay out one assumption to help you better understand the thrilling and exciting world of accounting.

The calendar is a crucial concept in the world of accounting, finance, and taxes. Due dates and deadlines reign supreme. The numbers you report on your tax forms are within the context of the tax year, or you’re paying tax estimates based on the previous quarter.

The calendar is to accounting and finance what time is to musicians. Musicians work within various time measures. Musicians think in tempo, bars, and beats per measure. Accountants and finance professionals think in months, quarters, years, in terms of due dates, and in reporting periods. Both worlds are ruled by time.

What Is Tax Planning?

Tax planning is simply meeting with your accountant at a minimum once a year, towards the end of the year (typically November or December), or more frequently (typically once a quarter) to review your business financials in the context of taxes.

Tax planning requirements

Here are the requirements your organization must meet in order to conduct tax planning meetings with your accountant effectively.

- You obviously need to have an accountant. Less obviously, you need an accountant who is willing to include tax planning meetings as part of their service package, and you may need to request this service.

- You must keep regularly updated bookkeeping records. This means that the books are closed and reconciled on a monthly basis. At its core, the act of bookkeeping is assigning categories to all your business transactions (revenue and expenses). Bookkeeping produces reports (your profit and loss statement, balance sheet, and statement of cash flows). And these reports are used to file your taxes. It’s helpful to give your accountant access to your books. Otherwise, you (or your bookkeeper or business manager) will need to perform additional administrative tasks to provide them with the data and reports.

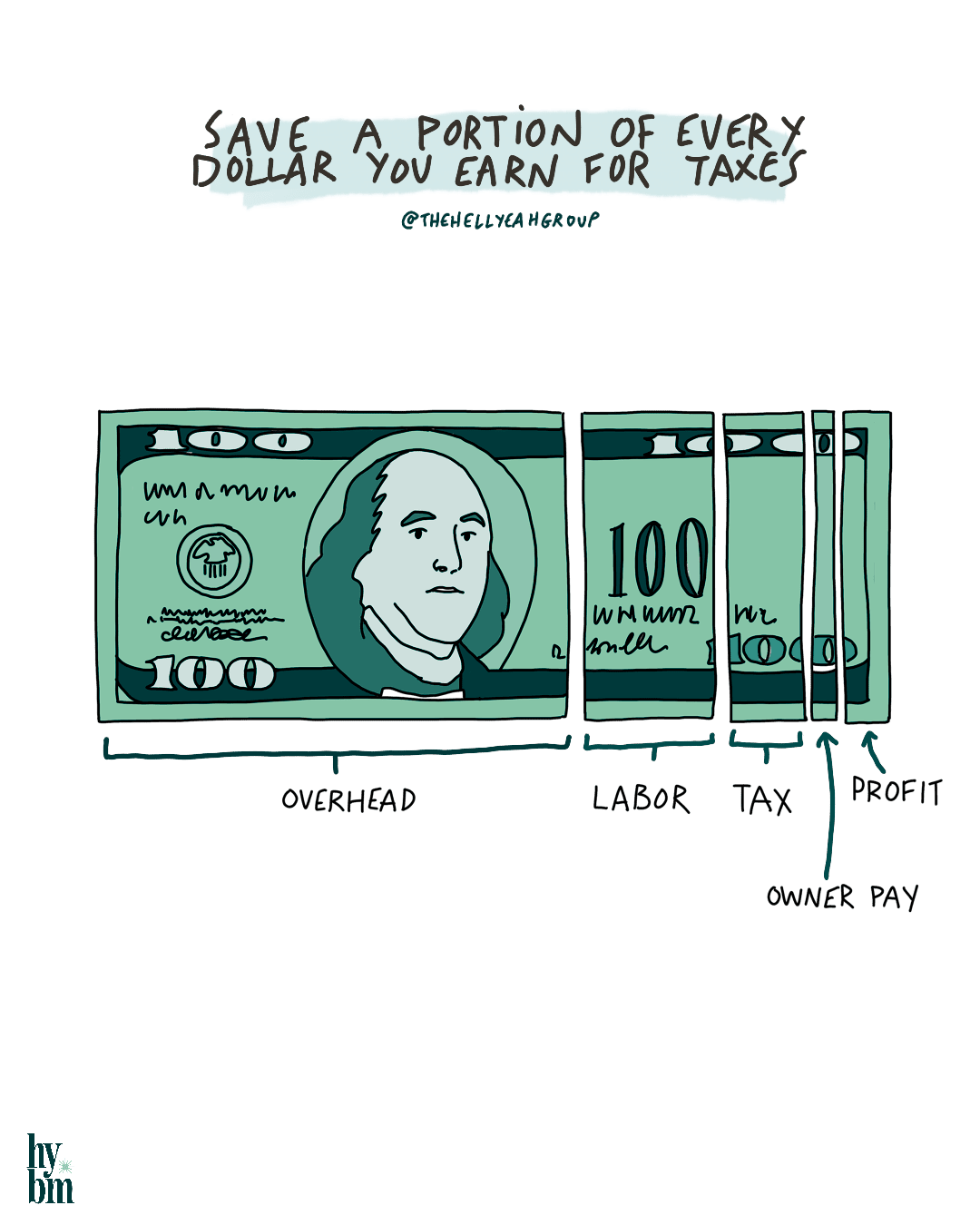

- It’s in your best interest to save a portion of every dollar you earn for taxes.

While it’s not a requirement, saving for taxes as you earn revenue is very, very, very helpful so that when you pay taxes (quarterly, annually, and when you run a year-end payroll), you already have the money set aside.

It’s generally accepted to save a portion of every dollar your business earns in a tax savings account. It’s generally acceptable to save between 10% and 30%. Some people do save as much as 40%. There are different ways to accomplish this logistically. There are bank accounts that automatically set aside a reserve balance as a percentage of every deposit. Or you can sit down each week or every other week to do the manual transfers.

What Is Year-End Tax Planning?

At a minimum, business owners should meet with their accountant once a year for year-end tax planning. This typically occurs in November or December.

I know you don’t want to ruin your holiday season by jamming a tax meeting in there, but you want to meet with your accountant before the tax year ends, especially if you’re like most creative businesses using the cash basis accounting method. 1

Remember when I mentioned earlier that the calendar rules the world of accounting and finance? The reason why we meet with our accountants towards the end of the year is because most of the tax year (which most likely coincides with the calendar year), is complete. So, when you meet with your accountant at the end of November, you will have 10 to 11 months of actual accounting and financial data, and then you’ll provide your accountant with an estimate of what you think the last couple of months will look like financially. From there, they will create a tax projection for you.

A tax projection is an estimate of what you’ll owe (or receive as a refund) come tax day. It’s a forward-looking way to estimate how much you’ll owe based on your expected income, expenses, and any tax benefits you may receive. Think of it as a sneak peek of your tax future. In contrast, filing your tax return is more like looking in the rearview mirror at what has already happened financially. Getting this preview helps you avoid unpleasant surprises, make smarter financial decisions, and plan ahead for when those tax bills are due.

A good accountant will also work with you to make suggestions about ways you might be able to legally reduce your tax liability through methods like making a retirement contribution, accelerating expenses before the year ends, deferring revenue until the following year, making a charitable contribution, and more.

S-Corps and Payroll

S-Corps are pretty cool because they often are one of the most efficient ways to structure a small business from a tax perspective. 2 But there is no free lunch, and that benefit comes at a cost. The owner of an S-corp that also works for the company, which is typical for many creative businesses, must legally run a payroll to pay themselves a reasonable salary.

Some accountants advise their clients to set up a regular monthly payroll and pay themselves a reasonable salary. Many other accountants advise their clients to pay themselves monthly (or semi-weekly) via a draw3. Then, at the end of the year, they run one payroll to “true up” a reasonable salary amount and pay into payroll taxes. This is also a strategy used if the income in your corporation is inconsistent and you aren’t sure what a reasonable salary is until you have gone through the majority of the tax year. If you’re like many individuals in this category, a year-end tax planning meeting is crucial to ensure you run your payroll and remain compliant.

What Is Quarterly Tax Planning?

Quarterly tax planning is typically less in-depth and extensive than the year-end meeting. This is partially because it’s not as easy to strategize when so much of the calendar year is in front of us. In other words, in the first and second quarters, there are still half a year of revenue and expenses that we can predict, but are ultimately uncertain about.

A quarterly tax planning meeting could simply look like your accountant reviewing your financials (your bookkeeping, which produces your financial statements) for the quarter and year to date. Then, they email you their recommendations, such as “pay this amount” as a quarterly estimated tax payment. You may also have a brief 10-minute phone call to discuss any additional details or questions you may have.

Of course, it could be more involved than that. Let’s say, for example, you are one of four business partners set up as an LLC. The ownership, workload, and personal expenses are not split equally. Quarterly tax planning necessitates a more detailed discussion in this context.

Use Our Tax Projection Tool

We’ve created this Tax Projection Calculator to help visualize what a tax projection looks like and does. This interactive tool illustrates how various income streams, deductions, and business decisions impact your potential tax liability. The calculator provides a simplified preview of what your accountant might prepare during your tax planning meetings.

Keep in mind that this calculator is strictly for educational purposes. it’s designed to help you understand the components of a tax projection and why year-end planning is so valuable. While it can give you a general sense of potential tax scenarios, it should never replace professional tax advice from your accountant who understands your specific financial situation and can recommend legitimate strategies to optimize your tax position.

Use our calculator below to run a tax projection. You can also click here to open the calculator in a new window.

How Tax Planning Saves You Money

Regular tax planning meetings with your accountant can save you money in the following ways:

- Avoiding penalties and late fees by staying on top of filing deadlines and quarterly payments

- Identifying legitimate deductions you might otherwise miss (especially with regard to any recent tax code changes)

- Making strategic decisions about when to make significant purchases or recognize income

- Taking advantage of retirement contribution options that reduce your taxable income

- Implementing strategies specific to your business structure to minimize tax burden

- It forces you to keep your bookkeeping up to date, so you aren’t wasting time and money trying to rush and finish it before tax day.

The most expensive mistake is not having this conversation at all. I’ve seen creative business owners save thousands—sometimes tens of thousands—simply by planning ahead rather than scrambling at the last minute.

How We Support with Tax Planning

We support our clients with tax planning across all of our service packages. From simple reminders to schedule tax planning meetings to comprehensive financial preparation, our goal is to ensure you’re never caught off guard by tax obligations. Our team can:

- Help maintain your books in an up-to-date and accurate manner throughout the year

- Prepare the financial reports your accountant needs for effective tax planning

- Set up systems to ensure you’re saving adequately

- Assist S-Corp owners with year-end payroll

- Create custom reporting that helps you track your tax obligations

While we don’t provide tax advice or file your income taxes, we work collaboratively with your accountant to ensure you have all the financial information needed to make strategic tax decisions for your creative business.

Remember, the most expensive tax mistake is not planning at all. By incorporating regular tax planning into your business practices, you’ll not only avoid penalties and surprises but potentially save thousands of dollars each year.

Footnotes

- Accounting Basis: There are two primary accounting methods businesses use. Cash basis accounting and Accrual basis accounting.

Cash basis accounting records revenue when payment is received and expenses when they are paid. For example, when you pay for an item at the store. If the store uses a cash basis accounting, it will record revenue received when the cash is deposited into the till. Accrual basis accounting records revenue when it is earned and expenses when they are incurred, regardless of when cash changes hands. For example, you hire a magician to perform at your birthday party in 3 months, and you pay in advance. The magician works for a larger organization that is using accrual basis accounting, so the company will not recognize the revenue until the magician performs. Yes, accrual accounting is administratively more demanding, and it requires a lot of communication between the accounting department and the rest of the organization to ensure the records are accurate.

Most creative businesses use cash basis accounting, while larger organizations and nonprofits often use accrual for more accurate financial reporting. ↩︎ - Use our Entity Tax Comparison Calculator to run hypothetical examples that help illustrate the various tax implications of different entity structures for small businesses. You’ll see that at certain income levels, the S-corp is often the most efficient from a tax perspective. But it’s not always the case, and it depends on your personal tax situation. So while the calculator is fun (!), and helps illustrate differences in business structures, it’s not a replacement for professional tax advice. ↩︎

- In an S-corporation, an owner draw (or shareholder distribution) is essentially a way for S-corp owners to withdraw money from their business beyond their salary.

Here’s how it works:

S-corp owners typically pay themselves in two ways:

1) A “reasonable salary” through payroll (which is subject to payroll taxes)

2) Distributions/draws (which are not subject to self-employment taxes)

Unlike regular salary payments, owner draws:

1) Are not subject to payroll taxes (Social Security and Medicare)

2) Are reported on your personal tax return since S-corps are pass-through entities

3) Can be taken regularly (like monthly) or periodically

It’s important to note that S-corp owners who work in their business must legally take a “reasonable salary” before taking distributions. This is a common area where business owners often encounter tax issues.

Taking only distributions without a reasonable salary can trigger IRS scrutiny, as it could be seen as an attempt to avoid payroll taxes. ↩︎