The Most Common Financial Mistakes Creative Businesses Make: Cash flow model? Never heard of her.

By Paco De Leon

Welcome to the third installment in our series where we’re examining the most common financial mistakes that creative businesses make.

In our previous posts, I debunked the expensive myth of the Delaware C Corp and explained how proper tax planning can save you thousands. Now, we’re tackling another critical aspect of financial management: knowing your cash flow.

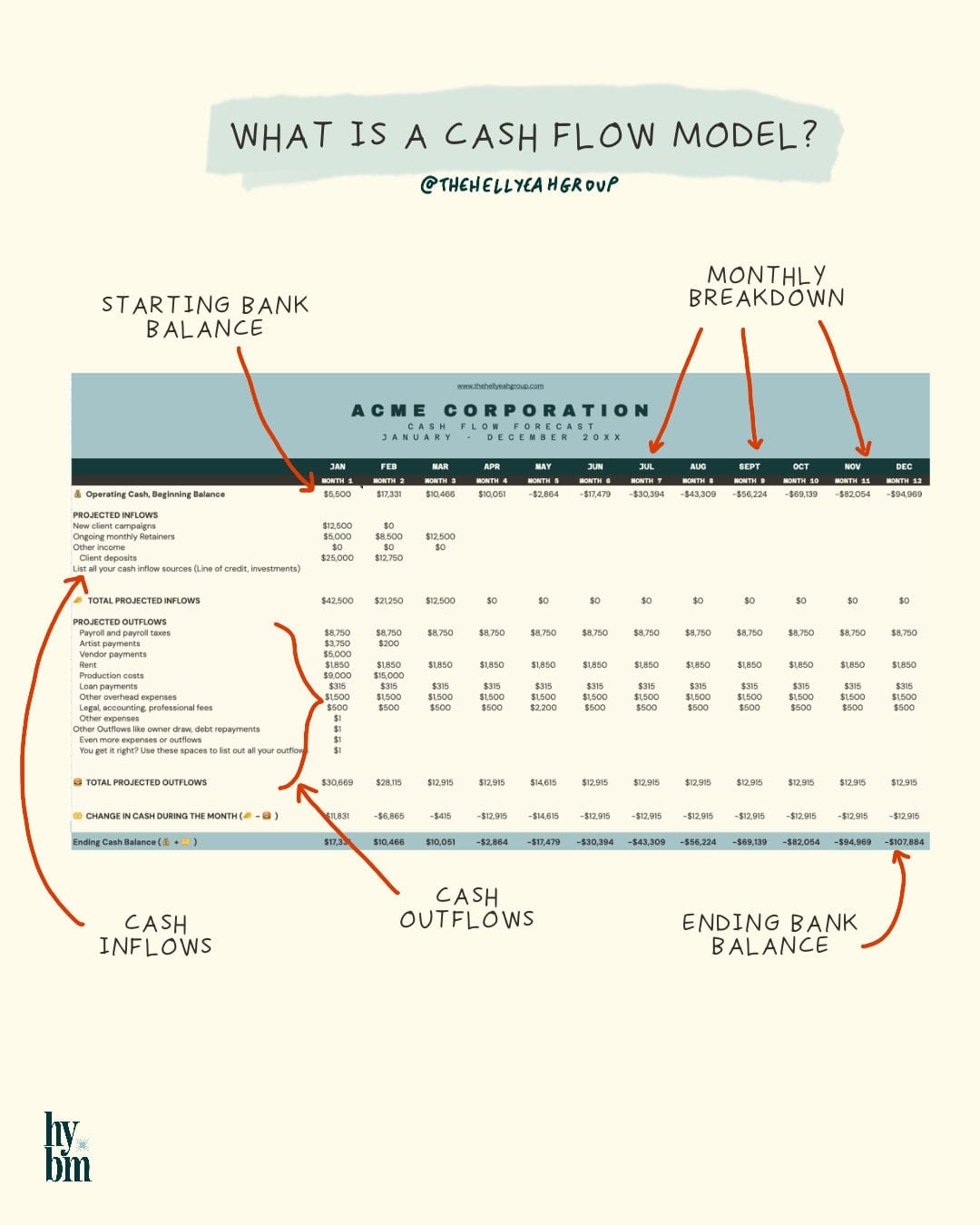

What is a Cash Flow Model?

Throughout this post, I’ll use the word cash flow to mean cash flow projections or a cash flow model. While it sounds complicated, it’s ultimately a spreadsheet that shows you your business from a forward-looking perspective. Here’s what you’ll see in a cash flow model.

- Monthly Breakdown

First, the reference point is monthly. - Starting Bank Balance

At the top of each month, the model starts with the cash balance at the beginning of the month. The cash balance may be a checking and savings account. Sometimes the balance is an aggregate of several cash accounts. - Cash Inflows

Next, you’ll see projected cash inflows in the form of revenue. Some models might even list other non-revenue inflows here, like an owner investment or cash coming in from a line of credit. For our models, we put these at the very bottom, near the ending cash balance. - Cash Outflows

Then come projected outflows. First, you’ll see your Cost of Goods Sold (COGS) or Cost of Services — these are the direct costs of delivering your service — the expenses that wouldn’t exist if you didn’t perform the service. For example, After COGS, you’ll see your projected operating expenses. Then you’ll see any additional projected outflows like loan repayments, tax payments or owner draws. - Ending Cash Balance

Finally at the bottom, you’ll see the projected cash balance at the end of the month.

Why Do You Need a Cash Flow Model?

The goal of a cash flow model is for business owners to understand what their cash balances will be month over month. This is essential for agencies with varied monthly revenue and clients who may take anywhere from 60 to 120 days to pay their invoices. Understanding your projected cash flow helps you anticipate potential cash shortages, plan for expenses, and ensure you can meet payroll and vendor payments even during periods of delayed income.

But Paco, if I have If do my bookkeeping in QuickBooks, do I really need a cash flow model? I’m glad you asked.

The Problem with Accounting

There are two big problems: bookkeeping and accounting are backwards looking and are a compliance requirement, not necessarily a tool for entrepreneurs.

While these systems are essential for filing your taxes, their primary focus is reporting what has already happened rather than helping you plan for the future. Most bookkeeping software will tell you what money came in and went out, but won’t help you understand if you’ll have enough cash to meet next quarter’s payroll or handle an upcoming tax payment.

This backward-looking nature of traditional accounting is precisely why creative businesses need cash flow models. Your profit and loss statement might show you’re profitable, but if your biggest clients take 90 days to pay while your expenses are due monthly, you could still face serious cash shortages.

Profit is not cash

Remember: creative businesses don’t die because they’re unprofitable – they die because they run out of cash. A cash flow model gives you the forward-looking perspective necessary to avoid this common pitfall.

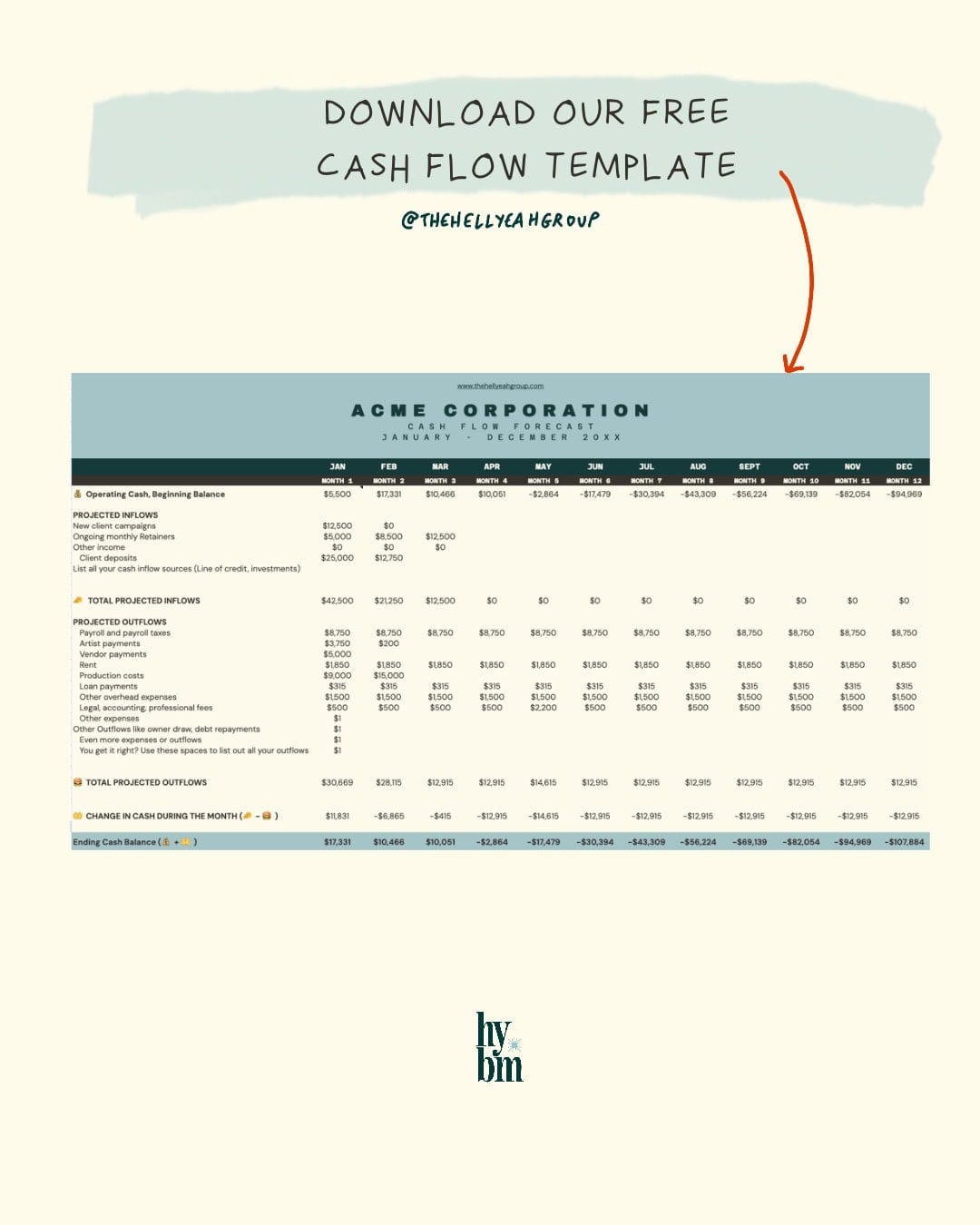

Build Your Cash Flow Model with Our Template

Hopefully, we’ve convinced you that you need a cash flow model. Instead of building yours from scratch, use our simple template to get started here.

Building a cash flow model is a lot like building a budget. You’ll want to make sure to project when you expect revenue to land in your bank account and when you expect to incur expenses. Don’t forget about large one-time expenses like an annual subscription or a draw for quarterly tax payments.

What Your Cash Flow Tells You About the Health of Your Business

Looking at cash flow projections can help you understand the health of your business from the particular perspective of cash. This is wildly important because if you are a growing creative business, you need cash on had to say to new projects, to pay your employees and contractors, to invest in more marketing activities that get you more clients and keep you on this beautiful and ridiculous hamster wheel of entrepreneurship. Not to mention, you need cash to keep the figurative and literal lights on.

Here are some common things your cash flow model might be telling you and solutions and possible solutions.

1. You have cash flow timing issues.

This is by far the most common thing we see among creative businesses. It’s not that your business isn’t making money or a profit. It’s the painful cash flow gap between when you pay contractors and employees for their services and when your clients pay you. If you’ve worked with a big corporate client or major studio, you know this problem intimately.

Since there’s not a snowflake’s chance in hell that you can change the payment terms because they are a Goliath and you are a beautiful little David (even though David blinds that bitch in the end). You, like all their other creative vendors, must bend the knee and accept their terms.

Best way to combat this common issue is to have access to capital (cash) before you need it. Key words here are before you need it. So what does that look like?

There are several ways to address cash flow timing issues in your creative business:

- Build up savings on hand. While this approach takes time to build up, it can feel less risky than alternatives. While having to use your savings can feel painful, and there’s an opportunity cost to keeping your cash in savings rather than investing it elsewhere in your business.

- Apply for a line of credit or a factoring loan. The advantage here is that you can apply before you actually need the funds. Though borrowing money might feel risky, and maintaining a line of credit costs money even when you don’t use it, this option ties up less of your own cash that you could be using to operate or invest in your business.

- Diversifying your revenue with more clients can help balance cash flow. However, this isn’t a perfect solution—while more clients can reduce dependency on any single payment schedule, managing additional client relationships brings its own challenges. Growth often requires money to bid on projects and to pay contractors for more work.

2. How Much You Can Afford to Invest In Your Business

Running different scenarios is the second most common use case for how we help our clients using cash flow models.

From how much more can they invest in marketing to how a new hire will impact their cash. For the latter example, employee costs are isolated in a separate line item. In future months, we add in new hires to see how that will impact cash going forward.

Let’s say a client wants to hire a new producer at a $95,000 salary. We can see how that additional cost (including taxes and benefits) will impact cash every month.

Sometimes we learn the company can afford the decision and it will open up the partners to do more business development to get more clients. Other times, we’re faced with the reality that delaying our new hire by 3 months would be the more sustainable choice.

3. Your Business Is Vulnerable (or Unsustainable)

If your model reveals constant cash flow problems that can’t be chalked up to issue of timing, you might have to confront the reality that the current way you’re operating your business needs to change.

There isn’t one universal diagnosis for this issue. It could be that your costs have simply gone up over the years, while your pricing, offering or growth did not keep up. And once you see the different levers that can be pulled up or down, it’s a matter of coming up with a plan and executing it.

How We Support Clients with Cash Flow Management

We build and maintain cash flow models for our clients. These models provide clarity on what’s coming in and what’s going on. And most importantly, what their cash balances will be in the coming weeks and months.

We meet with our clients on a monthly cadence (sometimes as frequently as weekly). During these meetings, we review the monthly cash flow. And we also make adjustments for future months.

Cash flow meetings facilitate business decisions. And to answer questions like “how much can we afford to pay this person,” or “Can I take the next 4 weeks off and not bring in any new business?”

You get access to your cash flow (along with various other live reports) in a shared Google Sheet. And, of course, we’re available to answer questions outside of monthly meetings, so long as it’s within reason.

Interested in this kind of support? We’d love to connect to learn more about your business.