How To Articles

A Christmas Carol tells the story of Ebenezer Scrooge’s redemption. Our main character, Scrooge, starts as a cranky old man who hoards his wealth, treats his employees like garbage, and bums people out with his bad vibes and lack of generosity. Throughout the story, we bear witness to Scrooge’s transformation. He is visited by the ghosts of Christmas past, present, and what is yet to come. These spirit guides help Scrooge slowly gain clarity on who he has been and wants to become.

Through these visions, Scrooge recognizes the error of his ways, and by the end, old Ebenezer finds the willingness to change. If you haven’t read Charles Dickens's novella, I’m sure you’ve seen some version of it. Some old 90’s sitcoms have used this same framework to help the hero of a story emerge on the other side a better, more aware version of themselves.

Weirdly, the work we do at Hell Yeah Bookkeeping is a bit like this story. Thankfully, our clients aren’t cranky old misers. Instead, they tend to be insightful, creative business owners. And they need our help to become better, more aware captains of their company. In perfect conditions, we take our clients through a similar, but less dire, Scoorge-like journey where the ghost of business-past, business-present, and business-future all help our heroes have clarity and inspire a change to be better business owners.

Here are all the lessons I’ve learned from all the business owners with whom I’ve had the pleasure of working. They helped me build my sustainable business first by being paying customers, but I’ve also had the unique viewpoint of watching them grow their businesses from the inside out. Watching and playing a tiny, supporting role in other people’s success has been really fun.

Lifestyle creep happens when two things in your financial life increase: your income and your spending. Specifically, lifestyle creep happens when you spend your extra income on things that upgrade your lifestyle; as opposed to maintaining your current lifestyle after your income increases.

Welcome to part 2 of “The Lazy Person’s Guide to Building Wealth.” If you missed part 1, get caught up here. If you’ve ever been curious about investing in the stock market but are honestly puzzled about how to get started, this guide is for you. If you question whether investing in the stock market is a realm reserved only for Wall Street moguls or the already rich, this guide is also for you. By the end of it, you’ll have everything you need to know to start investing.

Navigating the intersection of love and money can be tricky, especially if one partner is more of a spender than the other. There is one method of managing finances that can help every couple find the balance between working towards the same financial goals, while also maintaining some level of autonomy. It’s called “splitting the check.”

We don’t always get what we give. At least, that’s what the Italian economist and sociologist Vilfredo Pareto discovered in the 1800s while harvesting peas from his garden. Pareto observed that 80% of the peas came from only 20% of the peapods, demonstrating an unequal relationship between inputs and outputs. Wondering if this pattern would repeat itself in other areas of life, Pareto began to look at different data sets to confirm his findings.

While this principle might skew and not always hold one hundred percent of the time, the general principle that 80% of effects result from 20% of causes holds. Less than 10% of the population owns 80% of the stock market. Few social media accounts are responsible for most misinformation across platforms. And we’ve recently seen, in a pandemic, that roughly 20% of the most infectious individuals are responsible for 80% of the transmission.

Knowing 80% of your success and results come from only 20% of your efforts; you can apply the 80/20 rule to your financial lives. Here are the five financial rituals you can focus on that will impact results the most.

What you need to know to learn how to maximize benefits and get the open enrollment help needed to have a health benefit plan that will work for your needs

The end of a year is a time for reflection. As you plan your end-of-the-year celebrations and start to plan your new year resolutions, you may want to consider taking some time to take a closer look at your finances. A year-end personal money review can help you reflect on the choices you made over the previous year and help guide you to make better financial choices in the new year.

Let’s take a look at what a year-end personal money review is and how it can help you have a better relationship with money:

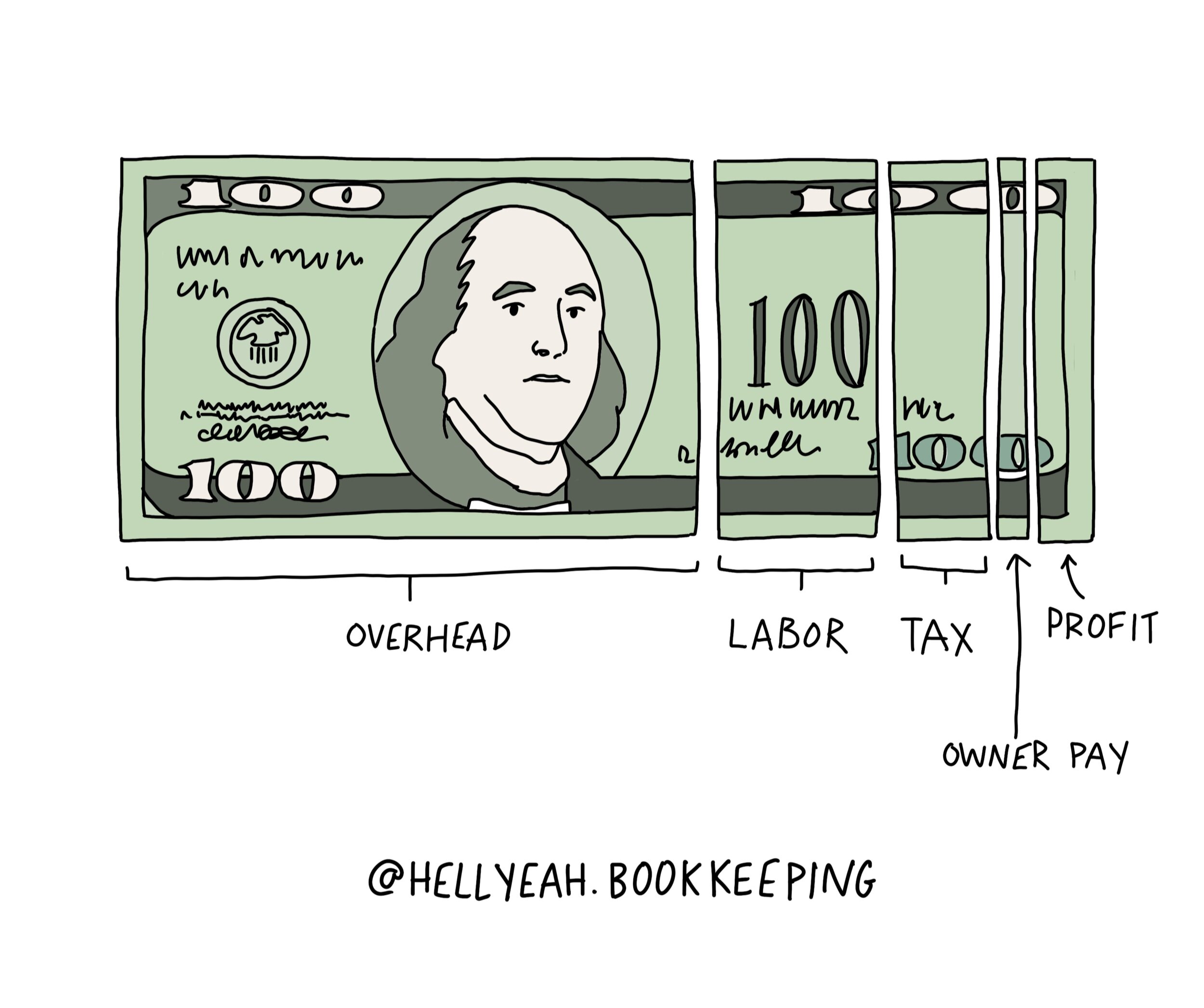

Do you know how much it costs your business to earn each dollar it makes? Unlike traditional employees, when you're a self-employed service provider, every dollar you earn has a cost beyond your time and energy. How much do you need to pay for employee payroll, taxes, operating costs like marketing and insurance, profit, and personal pay?

Even if you’re a one-person freelance practice, understanding how much it costs you to earn each dollar in your company is a valuable shift in perspective that can help you build a sustainable, efficient business.

Even if you have all the right practical, rational information, when you're in a state of fear, anxiety, or stress, it is impossible to make sound, rational decisions. These states are innately emotional states where cognition is bypassed. When you're afraid, a part of your brain (amygdala) releases hormones that prepare your body for a "fight or flight" response. Humans struggle with having control when we're in these states because the amygdala has few connections to the rational parts of our brain, like our cortex.

So you’ve discovered that tax saving wonder known as the S Corp. You’re ready to start kicking the tires by learning what this “Reasonable Salary” thing is all about. Let’s discuss what it means, why it matters, and the best way to find yours.

A reasonable salary for an S Corporation's shareholder-employee is the part of their compensation that must be treated as employee wages. The IRS requires you to be paid an appropriate wage for the services you provide your corporation because provides needed funding for Social Security and Medicare. It’s best to work with an experienced tax professional to set your optimal reasonable salary, but this article will be a great primer to get acquainted with what a reasonable salary is.

In 1930, John Maynard Keynes, who is considered the father of modern economics, wrote an essay titled, Economic Possibilities for Our Grandchildren. In that essay, he describes his prediction for what life would be like for future generations. He predicts that economic prosperity will be so great and abundant that our need to work across all of society will diminish. And since the vast majority of people will no longer need to "sell themselves for the means of life," he warns that humanity's next great challenge will be how to look forward to and not dread the "age of leisure."

While he predicts there will be some people who have an "intense, unsatisfied purposiveness" that causes them to continue to pursue wealth blindly, he goes on to imagine that the vast majority of society will have a shift in moral codes. That we will recognize that loving money as a possession, as opposed to as a means for the realities and enjoyments of life, will finally be collectively viewed in the harsh light of truth; that it is disgusting, morbid, semi-pathological and semi-criminal.

Imagine that your financial life is a sandcastle you’re building on the beach. You can learn what works for building it up, and in the good times, when the threats to your progress are manageable, you take for granted that it’s easier to build in those conditions. Now imagine the tide rising, the waves start coming in, getting closer and putting your sandcastle in danger of being damaged or worse, being washed away. In this analogy, the tide is a financial shock. The thing about the tides - and economic shocks - is they will always come in. Sometimes very quickly and suddenly as if out of the blue and other times, you can feel it gradually creeping in. Experiencing a financial shock is not a matter of if; it’s a matter of when and to what severity. Shocks can come in the form of global recessions, pandemics that freeze the economy, you lose your job, your kid getting very sick, a parent dying, the industry you’ve worked in for decades slowly getting cannibalized by new technology or war.

In the financial world, we call things like the current pandemic a black swan event. A black swan is an unpredictable event with potentially severe consequences. The name comes from the rare sightings of black swans in nature. They exist, but seeing them is exceptional. So while the financial world has terms for these types of events, how we deal with them isn't always the same. Take the 2008 housing crisis. It was the result of a perfect storm of things: sub-prime mortgages, derivatives, hubris, and the lax, or often fraudulent practices within the real estate, mortgage and lending sectors. Finding a way out of the crisis was terrifying, but pointing to the causes gave us a sense of certainty.

I want to be clear: what we're experiencing today is very different from the housing crisis of 2008. Although there is one similarity: we didn't have a playbook for dealing with the crisis then, and it goes without saying, we don't have one today. While it's true, the world has experienced pandemics in the past, our modern economy, in all of its globally connected glory, has not experienced something of this scale. I have no idea what is to come in the approaching days, weeks, or months. I'll do my best to help you all understand our changing reality through the lens of money, finance, and economics.

Here are my thoughts on how to not freak out about your finances during a global pandemic.

Bookkeeping isn't that fun. Seeing how much money your business made and watching profitability grow can be fun. But the actual act of accounting is mildly satisfying, at best, and frustrating to the point of tears, at worst. Even though bookkeeping software has become user-friendly, you still might end up making costly mistakes if you don't have some accounting chops to help you understand how to troubleshoot and fix things.

It's probably time to outsource your bookkeeping if any of the following are true:

You've tried to set up your chart of accounts, only to quit after getting stuck deep inside a Google hole.

You can't figure out why the bank balances don't match, and so you never reconciled your accounts.

Your business is doing so well that you don't have time to sit down and focus on the bookkeeping.

Written by Luke Frye

Tax time is coming again — you can feel it, can’t you? Like a vibration on a train track.

It’s unstoppable, yes, but that doesn’t mean you have to be flattened. Learning about how to handle your taxes is the best way to avoid a nightmare scenario. The good news is that there are some basic principles, and it doesn’t take a wizard to learn them.

Here are four ways to have a smooth tax season, no locomotives involved.

Everything is connected. Your relationship with money impacts both your inner world and your external world. In your outer world, outside of you, your feelings about money can impact how you see the world, how you act in the world, and how you interpret experiences in the world. In your inner world, your relationship with money can impact how you feel. You cannot wholly compartmentalize your financial life; as much as you may have convinced yourself you can. How you feel about your financial life and your relationship with money, impacts how you feel about yourself. How you think about yourself affects the choices you make. And all the choices you make, create who you are, what you're able to do, and who you will allow yourself to be.

I moved to LA when I was 22, having just landed a job as an assistant at a boutique business consulting firm. Part of my job was driving around Los Angeles to run all sorts of errands. I'd deposit checks for clients at various banks all over town. I'd go to the post office to send tax returns via certified mail. I'd pick up lunch for the office, and go shopping for my boss. Keeping receipts for everything was easy. I didn't have very much responsibility, so whenever I got back in the office from one of my field trips, I had time to organize all the receipts. It was easy to make it a priority, especially when I had an employer who was in charge.

If you fast forward to recent years, I had gotten considerably crappier at keeping my receipts organized. For an embarrassingly long time, I was finding faded receipts at the bottom of my backpack or crumpled up in my back pocket, or the worst scenario of all - some would be lost and never found.

How many times have you thrown a penny away? Like you saw a penny on your desk, or you got it as a change, and instead of putting it in your pocket to use later, you throw it in the actual garbage? I'm not trying to judge you; I'm just trying to illustrate how the penny has lost its value over time.

In 1909, you could buy a copy of the New York Tribune for one cent. And in 1932, you could travel a mile in Southern Railway System. And I'm sure you might have heard a grandparent speak of buying candy at a local five-and-dime for a penny.

How does a penny go from getting you an entire newspaper to being so annoying that you'd rather throw them away than carry them around?

When money becomes less valuable, it's usually due to inflation.

People always assume I am so deeply passionate and stoked about finance. Like I jump out of bed and get excited about interest rates. That's not exactly true. I am super stoked and passionate about helping people, feeling like my work matters and having autonomy over it. So when people ask me why I started The Hell Yeah Group, the answer is often that, " I looked inside of my tool box of skills and realized I had some sharp tools that all pertained to bookkeeping, running a small business and personal financial planning.” As much as I wanted to create a cool company that had nothing to do with finance, I had constraints: I needed to earn money and there was no denying the skills I had, no matter how uncool I thought it was. Not exactly visions of grandeur, more like shining a turd.

But I’ve really grown to love how my work makes me feel, regardless of it’s non-passion status. I want to share the industry-specific things I’ve learned and observed over the years that I think everyone should know.

What do we want? Gratification!

When do we want it? Instantly!

We live in a world saturated in instant gratification. We can contact our friends through multiple channels at any time of day, from anywhere in the world. We can have the city’s best sushi or a even just single lime delivered to our front door. The amount of entertainment we have access to at our fingertips is a number that my brain cannot actually comprehend. And we can generate a rush of dopamine in the time it takes to write a caption for a photo.

It’s no wonder why we give up on the things that require more than a few minutes of focus. We have so many other ways to feel instantly good and to distract us from the real work we could be doing. But real work takes, well - real work.

I’m just going to come out of the closet and say this: I actually hate budgeting. And I think so many of us have sucked at it because it actually inherently sucks. A budget is the harsh fluorescent light the morning after, revealing all of our past personal mistakes. Not being able to stick to a budget highlights just how out of control we are in our daily lives, like how we are powerless to marketing that connects with us emotionally or how the market or an employer dictates what we can afford and ultimately, how we live our lives. On the surface, a budget is a bunch of numbers, but at it’s core, it forces us to confront ourselves.

Written by Luke Frye

Okay, this is going to sound extremely biased... but, as an accountant, I strongly recommend hiring a professional to file your business’s tax returns.

Sure, you’ll have to part with some of your hard earned cash in the short term. But I guarantee it will save you time and headaches. And if it helps you avoid making costly errors on your tax return (y’know, the ones that result in IRS fines), it’ll also save you money in the long run.

That said, I’m aware that it’s not always possible to hire a pro. So, if you’re doing your own tax return this year, here are some common mistakes to avoid.

Here are my predictions for what’s in store in 2024 and what that means for creative businesses. They’re a result of reflecting on the last year, observing larger trends and chatting with folks across various creative industries, from creators who make money on social media to to small business owners, artists, and folks in the podcasting industry. A lot of this may be anecdotal, but some of these patterns are worth paying attention to. Let’s dig in.